USDA Loans

Zero Down Home Financing

Buying a home doesn’t have to require a large upfront investment. For many buyers, finding a mortgage that minimizes out-of-pocket costs while keeping monthly payments manageable is key. USDA loans offer one of the most affordable paths to homeownership available today — with no down payment required.

At Johannsen Group, we help buyers understand whether USDA is truly the right fit by comparing it against options from 150+ lenders. For many, it can significantly reduce both upfront costs and monthly payments while keeping long-term financing stable and predictable.

What Is a USDA Loan?

A USDA loan is a government-backed mortgage supported by the United States Department of Agriculture. It is designed to help homebuyers purchase properties in eligible areas outside major urban centers.

Despite the name, many qualifying locations include suburban communities, growing outer-ring cities, and areas just beyond major metro centers. In practice, this allows many buyers to stay within a comfortable commute while still qualifying for the program.

Who Is a Good Fit for a USDA Loan?

USDA loans are ideal for buyers who:

Want to purchase with little or no down payment

Are open to homes just outside major metro areas

Have moderate household income

Plan to live in the home as a primary residence

Many buyers assume they won’t qualify due to income — but the limits are often higher than expected.

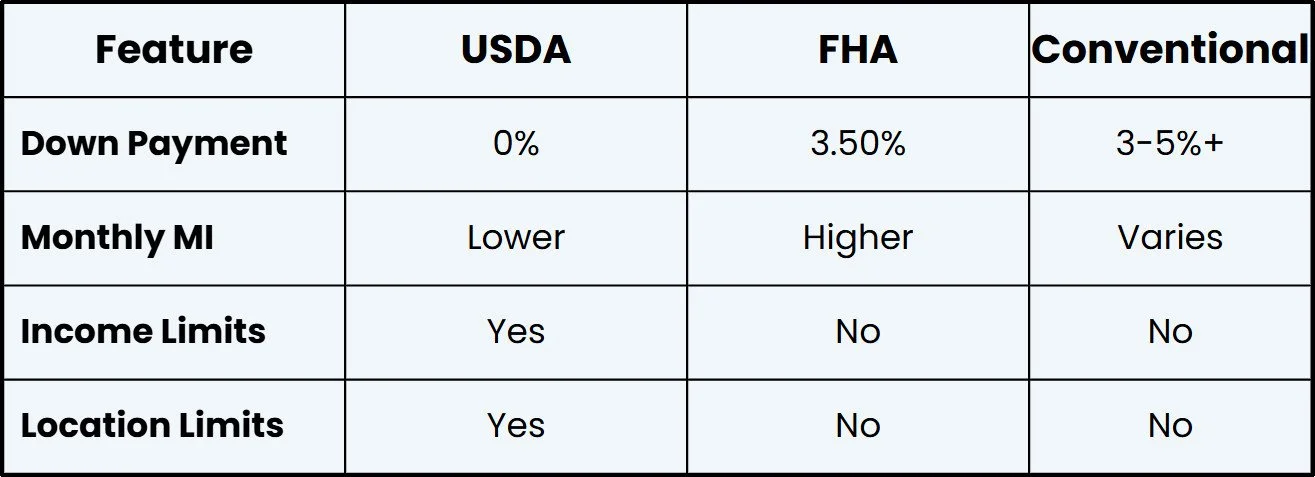

How USDA Compares to Other Loan Options

USDA Loan Requirements

Before applying, it’s important to understand the general eligibility criteria:

Income Limits

USDA loans have household income limits that vary based on location and family size. In many areas, 1–4 person households often fall roughly in the ~$110K–$120K range, with higher limits for larger households.

Property Eligibility

The home must be located in a USDA-eligible area, which often includes suburban and expanding residential communities.

Primary Residence Requirement

The property must be used as your primary residence.

Credit and Income Review

Lenders evaluate your credit profile, income stability, and overall financial picture.

Debt-to-Income Ratio (DTI)

Flexible guidelines apply, making it accessible for a wide range of buyers.

USDA Loan Limits

USDA loans are not structured around traditional loan limits like conventional or FHA loans. Instead, eligibility is based primarily on income and overall affordability.

Understanding this helps you:

Determine if your household qualifies

Identify realistic home price ranges

Compare USDA against other loan options

At Johannsen Group, we calculate eligibility precisely, including allowable adjustments that may improve your qualification.

USDA Loan Process

1. Pre-Approval

We review your financial profile and determine if USDA is a viable option.

2. Financial & Income Review

We verify income limits, gather documentation, and prepare your file.

3. Loan Comparison

We compare USDA with other loan options to ensure it provides the best overall outcome.

4. Home Search & Eligibility Check

We confirm the property meets USDA location and condition requirements.

5. Underwriting

Your file goes through lender review along with an additional USDA approval step.

6. Final Approval

You receive confirmed loan terms and closing details.

7. Closing

You sign final documents and move into your new home.

Key Benefits of USDA Loans

-

USDA loans allow eligible buyers to purchase a home without a down payment, removing one of the biggest barriers to homeownership. This makes it possible to move forward without needing to save a large upfront amount.

-

With competitive rates and reduced mortgage insurance, USDA loans are designed to keep monthly payments more affordable compared to many other loan options.

-

Because USDA loans are government-backed, lenders are able to offer stable and often lower interest rates, helping reduce long-term borrowing costs.

-

USDA loans include mortgage insurance, but it is typically lower than FHA, resulting in more manageable monthly payments over time.

-

USDA loans are designed for everyday buyers, with more flexible guidelines around credit, income, and debt-to-income ratios compared to conventional financing.

-

With the right loan structure and possible seller concessions, many buyers are able to significantly reduce their upfront closing costs, making homeownership more accessible.

Why Work with Johannsen Group?

USDA Loan Expertise

We help you understand whether USDA is the right fit by comparing it with multiple financing options.

Access to 150+ Lenders

We evaluate a wide range of loan programs to find the most cost-effective solution.

Full Financial Picture Guidance

We break down monthly payment, cash to close, and long-term impact — not just rates.

Clear and Confident Decision-Making

Our approach is focused on helping you make the right choice, not pushing a single loan program.

Start Your Conventional Loan Journey Today

A USDA loan can be one of the most cost-effective ways to purchase a home — especially if your goal is to minimize upfront costs and keep monthly payments low.

If you’re ready to explore your options or begin the pre-approval process, reach out to Johannsen Group today. We’ll help you confirm eligibility, compare loan options, and structure the best possible scenario for your home purchase.