Specialized Portfolio Loans

Flexible Mortgage Solutions for Unique Financial Situations

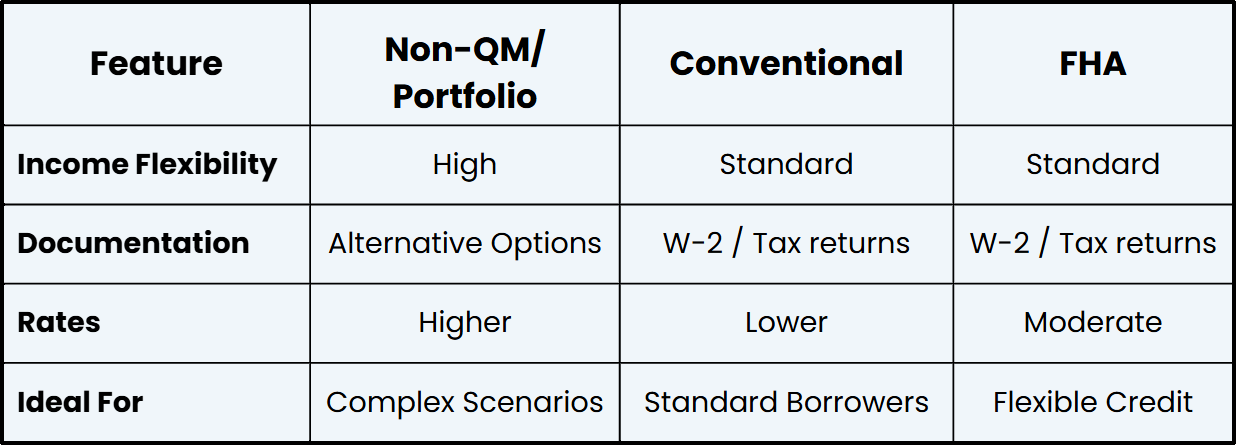

Not every borrower fits into traditional lending guidelines—and that doesn’t mean you shouldn’t have strong mortgage options. Portfolio and Non-QM loans are designed for buyers and homeowners with complex income, unique assets, or non-traditional financial profiles.

At Johannsen Group, we help structure these loans across 150+ lenders to find solutions that reflect your real financial picture—not just what shows on standard documents.

What Are Portfolio & Non-QM Loans?

Portfolio Loans

These are loans that lenders keep in-house instead of selling to Fannie Mae or Freddie Mac. This allows for greater flexibility in how your application is evaluated.

With portfolio loans, you may benefit from:

Greater flexibility in qualification

Customized underwriting decisions

A more detailed, nuanced review of your finances

Non-QM Loans

Non-QM (Non-Qualified Mortgage) loans do not follow standard qualified mortgage rules, allowing for alternative ways to qualify.

These are still fully underwritten loans but offer more flexibility in how income, assets, and overall risk are assessed.

Who These Loans Are Designed For

Portfolio and Non-QM loans are ideal for:

Self-employed borrowers with significant write-offs

Business owners whose tax returns don’t reflect true income

Real estate investors building or scaling portfolios

High-income borrowers with complex compensation (bonuses, commissions, RSUs)

Buyers with recent life changes such as career shifts or gaps

How This Compares to Traditional Loans

Portfolio & Non-QM Loan Requirements

Before applying, it’s important to understand general expectations:

Income Evaluation

Alternative documentation such as bank statements or asset-based qualification may be used instead of traditional tax returns.

Credit Profile

A solid credit history is still important, though flexibility may be available depending on the program.

Down Payment

Down payments are typically higher, often ranging from 10–25% or more depending on the loan structure.

Assets and Reserves

Lenders may require reserves or proof of additional financial stability.

Debt-to-Income Consideration

Flexible approaches are used, especially when income is calculated differently.

Common Loan Programs We Offer

Bank Statement Loans

Qualify using 12–24 months of bank statements instead of tax returns.

DSCR Loans (Investor Cash Flow)

Qualify based on the property’s income rather than personal income.

Asset-Based Loans

Use savings, investments, or retirement accounts to qualify.

1099 / Alternative Income Loans

Designed for independent contractors and commission-based professionals.

Is a Portfolio or Non-QM Loan Right for You?

1. Initial Review

We evaluate your full financial picture, including income sources and assets.

2. Strategy Development

We identify the most suitable loan structure based on your situation.

3. Lender Comparison

We compare multiple Non-QM and portfolio lenders to find the best option.

4. Documentation Collection

We gather the appropriate alternative documentation required for your loan.

5. Underwriting

Your file is reviewed with a more flexible, case-by-case approach.

6. Final Approval

You receive confirmed loan terms and closing details.

7. Closing

You finalize documents and complete your purchase or refinance.

The Loan Process

1. Initial Review

We evaluate your full financial picture, including income sources and assets.

2. Strategy Development

We identify the most suitable loan structure based on your situation.

3. Lender Comparison

We compare multiple Non-QM and portfolio lenders to find the best option.

4. Documentation Collection

We gather the appropriate alternative documentation required for your loan.

5. Underwriting

Your file is reviewed with a more flexible, case-by-case approach.

6. Final Approval

You receive confirmed loan terms and closing details.

7. Closing

You finalize documents and complete your purchase or refinance.

What to Expect (Tradeoffs to Understand)

These loans offer flexibility, but it’s important to understand the tradeoffs:

Interest rates are typically higher than conventional loans

Larger down payments may be required (often 10–25%+)

A strong overall financial profile is still important

Our role is to help you evaluate these factors clearly and determine whether this approach aligns with your goals.

Specialized Portfolio Loans

Frequently Asked Questions

-

They are simply structured differently and designed for non-traditional financial profiles. We help you evaluate if it’s the right fit.

-

Often, yes. Many borrowers use Non-QM as a temporary solution and refinance later.

-

Typically higher than standard loans, but it varies by program.

-

No. Many primary homebuyers use these loans due to income complexity.

Why Work with Johannsen Group?

Non-QM & Portfolio Expertise

You work with a team that understands how to structure flexible loan solutions based on real financial scenarios.

Access to 150+ Lenders

We compare multiple lenders offering different Non-QM programs to find the best fit.

Strategic Loan Structuring

We align your loan with your income, assets, and long-term financial goals—not just basic approval.

Clear, Guided Process

You receive straightforward, strategic guidance without confusion or guesswork.

Start Your Loan Strategy Today

A conventional loan offers flexibility, stability, and long-term value for a wide range of homebuyers. With the right guidance, you can secure financing that aligns with both your current budget and future goals.

If you’re ready to explore your options or begin the pre-approval process, contact Johannsen Group today. You’ll receive expert guidance, competitive loan solutions, and a clear path toward homeownership.